Builder Incentives on New Homes: What Buyers Should Know

Builder Financing Tricks: Why "Big" Incentives on New Homes Might Not Be the Deal They Seem

If you're shopping for a new construction home in Northern California and Nevada, Eastern Tennessee and surrounding areas, you've probably seen the headlines: builders offering massive rate buydowns, closing cost credits, or upgrades that look too good to be true? Should you pass them up? "Use our preferred lender and get 2% off your rate for years!" or "$15,000 toward closing if you finance with us!"

It feels like a win for buyers. But here's the reality many don't see until later: these incentives are often designed to keep the home's listed price artificially high while locking out outside lenders. The result? A micro-market where prices look stronger than they really are - and new developments that historically get hit hardest when the market cools.

At First Capital Mortgage Inc., we've helped countless families navigate new construction purchases across Northern California, Tennessee, Northern Nevada, and beyond. We want you to go in eyes wide open so you can truly get the best deal - not just the one the builder is pushing.

How Builder "Preferred Lender" Programs Work

Most large builders partner with one or more preferred (sometimes in-house or affiliated) lenders. In exchange for steering buyers their way, the builder offers special incentives - but only if you use that lender.

Common tactics include:

- Rate buydowns (temporary or permanent): The builder pays the lender upfront to lower your interest rate, sometimes dramatically, for the first 1 - 3 years or even the life of the loan.

- Closing cost credits or upgrades: Extra money toward your down payment, options, or fees.

- Lower earnest money or faster closing perks.

Legally, builders cannot require you to use their lender. However, they can and often do withhold the biggest incentives if you bring your own financing. Many buyers feel pressured to go along because the "big credit" looks like free money.

The Hidden Price Manipulation

Here's where it gets clever - and costly.

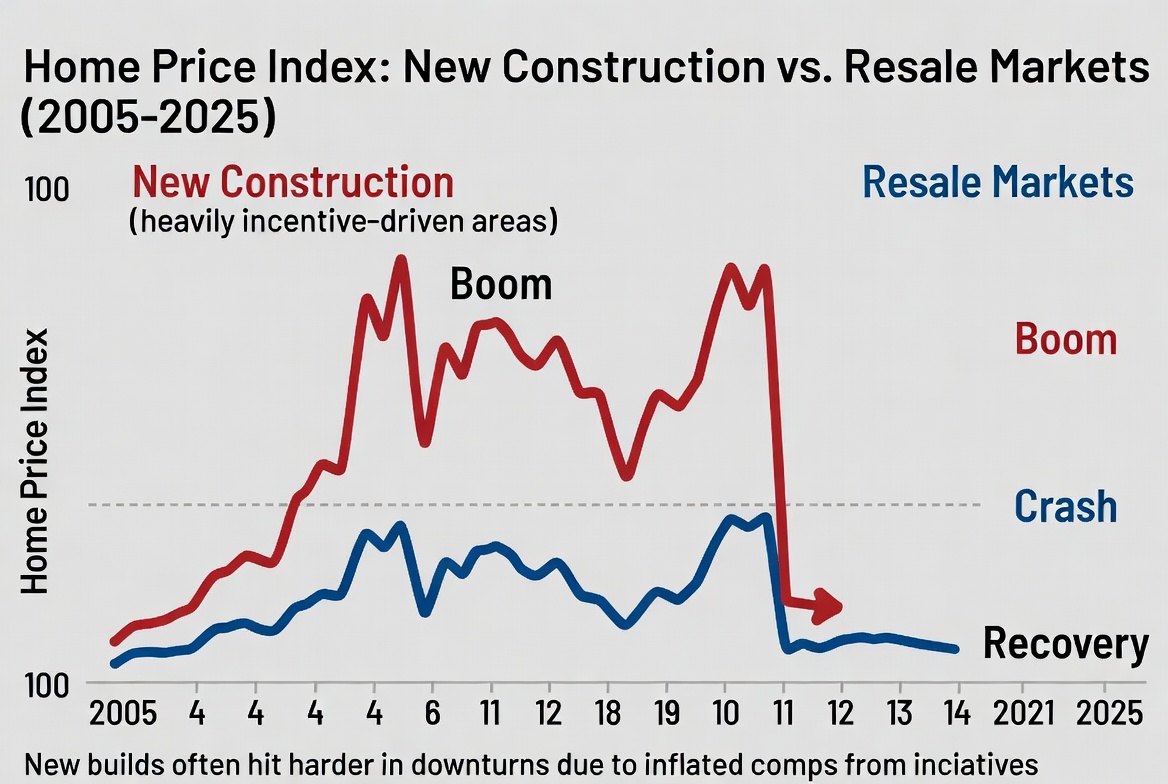

Builders hate cutting the sticker price on a home. Why? Because every price reduction becomes a comparable sale that can drag down values for every other home in the subdivision, including ones they haven't sold yet.

Instead, they keep the listed price high and use financing incentives to make monthly payments look more affordable. The buyer sees a "deal," but the actual sales price stays inflated. Those higher comps then support higher prices across the new neighborhood.

Result: the market in that micro-area looks stronger on paper than it actually is. Independent appraisers and outside lenders sometimes struggle to justify the value because so many recent sales were propped up by non-transparent incentives.

Buyers walk away thinking they won - only to discover later that they paid a premium for the home compared to what a straight price cut would have delivered.

Why This Backfires in Downturns

History shows the pattern clearly. Heavily developed new-construction communities - where builder incentives were common - have often been among the hardest hit when the market corrects.

When rates rise, incentives dry up, or buyer demand slows, those artificially supported prices can have farther to fall. Buyers who financed with big buydowns can face payment shock when the lower rate expires. And resale values can suffer because the "real" market price was never tested transparently.

We saw this play out in previous cycles: neighborhoods built during incentive-heavy periods often experienced steeper price drops and longer selling times than more balanced resale markets.

What This Means for You as a Buyer

You have options. You are never obligated to use the builder's lender. Here's how to protect yourself:

- Get pre-approved with an independent lender first, such as First Capital Mortgage Inc.

- Compare the builder's incentive offer apples-to-apples against what an outside lender can deliver on the same home price.

- Ask the builder if they'll still provide some concessions with outside financing - many will negotiate once they know you're serious.

- Run the numbers on total cost of ownership, not just the flashy monthly payment.

A slightly lower rate today that's tied to a higher purchase price can cost you tens of thousands over the life of the loan - and leave you with less equity if values soften.

Why Independent Lenders Like First Capital Mortgage Inc. Give You the Real Edge

We're not tied to any builder. Our job is to find you the best program - whether it's a conventional loan, FHA, VA, USDA, or one of the many first-time homebuyer options we specialize in. No hidden builder agendas, no pressure to hit their sales quotas.

We'll review your full picture, compare every incentive transparently, and help you decide if the builder's deal is truly the winner - or if bringing your own financing gives you more power at the negotiating table.

Ready to see what's possible without the strings attached?

Two Easy Ways to Start

- Complete our secure online application in about 15 minutes at www.promlo.com/mcneal.

- Or schedule a quick call or text us directly at 844-522-7100.

We'll pull a soft credit check with no impact to your score, review your options, and give you straight talk on how to approach any new construction deal - whether you're in Tennessee, Northern California, Northern Nevada, or elsewhere.

Homeownership should feel like a smart move - not a hidden game. Let's make sure you're getting the real deal.

Schedule a Consultation

Want a second opinion before using a builder's lender? Let's compare the real numbers and help you choose the option that protects your money and your future.

Start Your Pre-Approval

Get clarity before you negotiate with a builder. A strong pre-approval can give you more control and a better apples-to-apples comparison.

Click here to start your pre-approval for California

Click here to start your pre-approval for Nevada or Tennessee

Was this helpful?

If this article helped you better understand builder incentives and new construction financing, we'd be grateful for your review.

Questions about builder incentives or new construction financing? Drop them in the comments or reach out - we answer them every day.

- Your team at First Capital Mortgage Inc.

Helping families in Northern California and Nevada, Eastern Tennessee, and beyond build real equity, not just monthly payments.

References

- National Mortgage Professional - "Games Builders Play … And How To Beat Them" (2025). Discusses how builders inflate home prices to fund incentives while preserving comps.

- NewHomeSource - "The Pros and Cons of Accepting Builder Incentives" (2025). Covers rate buydowns and preferred lender programs.

- Zillow - "Builder Incentives Explained" (2026). Explains preferred lender incentives and rate buydowns.

- LendingTree - "Should I Use My Homebuilder’s Preferred Lender?" (2024). Notes that builders can offer incentives but cannot require their use.

- Silblawfirm - "Can a Builder Require You to Use a Certain Lender?" (2024). Overview of RESPA protections.

- HousingWire / AEI Housing Center analyses - Builder buydown strategies and their impact on apparent home values (various reports, 2023 - 2025).

- YouTube / Industry reports - "Home Builders Accused of Market Manipulation" discussions on incentives propping up prices.