High Federal Taxes? Mortgage & Tax Strategy Ideas

Are You Paying $50,000 or More in High Federal Taxes Each Year?

If you are paying $50,000 or more in federal taxes each year, your mortgage strategy may need to go beyond rate shopping. This article explores how high-income professionals, business owners, and real estate investors can start proactive conversations around tax planning, 1031 exchanges, energy-related tax credit strategies, and coordinated mortgage planning with qualified advisors.

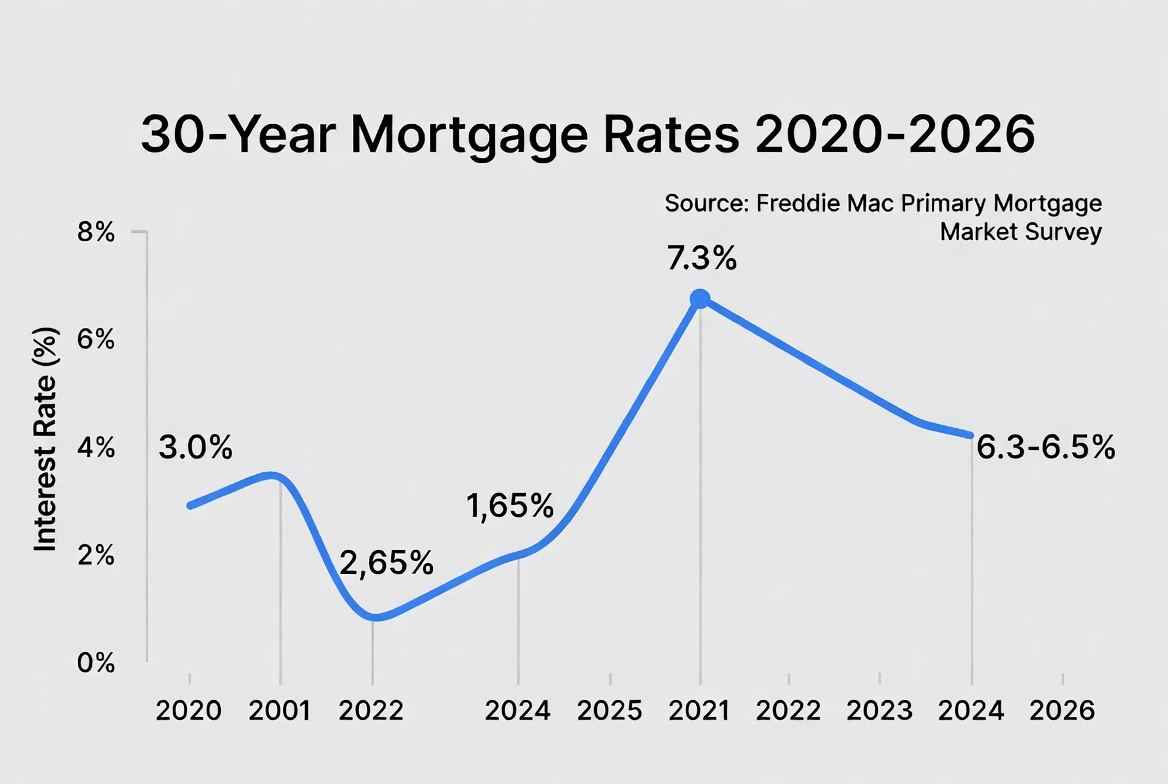

For many successful professionals, business owners, and real estate investors in California, Nevada, and Tennessee, 2026 has brought two important financial realities: mortgage rates remain elevated compared with the ultra-low-rate years, and many high-income households are still facing substantial federal tax bills.

If you are paying $50,000 or more in federal taxes each year, the conversation often needs to go beyond simply securing the best mortgage rate. The bigger question may be: Are you using every legitimate planning strategy available to protect more of what you earn and keep more capital working for your future?

As of late April 2026, 30-year fixed mortgage rates have recently been moving in the low-to-mid 6% range. That means today's best mortgage conversations are not just about rate - they are about strategy, cash flow, tax awareness, and long-term financial positioning.

Planning question: If your mortgage, investments, business income, and tax situation are all connected, when was the last time someone reviewed them together instead of separately?

What Tax Strategies Are High-Income Clients Exploring in 2026?

While every client's situation is different, two planning concepts continue to generate serious interest among high-income clients, business owners, and real estate investors we serve.

1. Energy Investments

Some high-tax payers are learning about structured investments connected to energy and clean energy projects. When properly structured, documented, and reviewed by qualified tax professionals, certain energy-related investments may qualify for federal tax credits or other tax benefits.

These strategies can be complex. Eligibility may depend on the type of project, ownership structure, placed-in-service date, financing, basis, passive activity rules, at-risk rules, depreciation treatment, and the taxpayer's specific income situation.

For that reason, this is not a "one-size-fits-all" recommendation. It is a conversation worth having with the right professional team if you are consistently paying substantial federal taxes and want to explore legitimate, documented strategies.

2. 1031 Like-Kind Exchanges for Real Estate Investors

Real estate investors often ask about ways to defer capital gains taxes when selling appreciated investment property. A properly executed 1031 like-kind exchange may allow an investor to sell qualified real property and reinvest into qualifying replacement property while deferring recognition of gain.

This can be powerful because it may allow more equity to remain invested instead of being reduced by an immediate tax bill. However, 1031 exchanges have strict rules, deadlines, qualified intermediary requirements, property-use requirements, and documentation standards.

If you own rental property, commercial property, land, or other investment real estate, a 1031 exchange conversation should happen before you sell - not after escrow is already closing.

Important: First Capital Mortgage Inc. does not provide tax, legal, investment, or accounting advice. We help clients review their broader mortgage and financial picture, and when appropriate, we can make warm introductions to experienced tax, legal, and financial professionals who can explain how these strategies may or may not fit your specific situation.

How Can Your Mortgage Broker Help with Tax Planning Conversations?

As your mortgage partner, we often see important parts of your financial picture: income, assets, liabilities, real estate holdings, business ownership, debt structure, and long-term goals. That does not make us your tax advisor - but it does put us in a unique position to notice when a deeper planning conversation may be valuable.

For example, a high-income borrower may be focused only on qualifying for a home loan or refinance. But when we review the full picture, we may also see questions worth exploring:

- Are you paying a large federal tax bill every year without a proactive strategy?

- Are you selling investment real estate and concerned about capital gains?

- Are you self-employed and showing strong income, but not coordinating mortgage planning with tax planning?

- Are you using debt, equity, and cash flow in a way that supports your long-term goals?

- Would a conversation with a qualified tax strategist help you see options you have not been shown before?

The conversation often starts with one simple question:

"When was the last time your tax professional brought you a proactive idea to lower your bill?"

Why This Matters for Business Owners, Investors, and High-Income Borrowers

Many successful people work hard, earn well, and still feel frustrated when tax season arrives. They may have a CPA who prepares accurate returns, but not necessarily a proactive advisor who brings forward planning ideas before the year is over.

That distinction matters. Tax preparation looks backward. Tax strategy looks forward.

If you are buying real estate, refinancing, selling investment property, expanding a business, or trying to reposition cash flow, your mortgage strategy should not be isolated from the rest of your financial life.

What would it mean for your family, your business, or your retirement plan if you could identify better ways to coordinate income, debt, taxes, and real estate decisions before the next tax bill arrives?

Ready to Explore Options That Go Beyond Your Mortgage?

If you are paying $50,000 or more in federal taxes annually and want to learn more about strategies others in similar situations are exploring, we invite you to start with a confidential conversation.

We will not give tax or legal advice. We will listen, review your mortgage and financial goals, and help you determine whether a deeper conversation with a qualified tax strategist may make sense.

Start the Conversation

Whether you are buying, refinancing, investing, or simply trying to make better financial decisions in 2026, First Capital Mortgage Inc. is here to help you think strategically.

Schedule a Confidential Consultation

Talk with Steve about your mortgage goals, tax concerns, real estate plans, and whether a strategic introduction may be helpful.

Start Your Pre-Approval

If you are considering a purchase or refinance, the first step is getting clear on your numbers.

Have a Tax Question?

If your tax bill is creating concern, let's discuss whether an introduction to a qualified tax strategist may be appropriate.

Helpful Mortgage and Tax Planning Resources

Related First Capital Mortgage Inc. Articles

External Authority Resources

Frequently Asked Questions

Can First Capital Mortgage Inc. give me tax advice?

No. First Capital Mortgage Inc. does not provide tax, legal, investment, or accounting advice. Our role is to help you review your mortgage and real estate financing options, then connect you with qualified professionals when a deeper tax strategy conversation may be appropriate.

Should I look at tax planning before buying or refinancing?

For many high-income borrowers, business owners, and real estate investors, it can be helpful to coordinate tax planning before major financial decisions. A mortgage, refinance, property sale, or investment purchase may affect cash flow, deductions, capital gains, liquidity, and long-term planning.

Is a 1031 exchange only for real estate investors?

Generally, 1031 exchanges apply to qualifying real property held for business or investment purposes. They do not typically apply to a primary residence sale in the same way. Because the rules are detailed and time-sensitive, investors should speak with a qualified tax advisor and qualified intermediary before selling.

Legal and tax disclaimer: This article is for educational purposes only and is not tax, legal, accounting, or investment advice. Tax laws and credit rules change, and eligibility depends on your individual facts and circumstances. Always consult your CPA, tax attorney, financial advisor, and other qualified professionals before making tax, investment, or real estate decisions.