Home Wealth Blueprint #2: Budgeting and Cash Flow – Know What You Can Comfortably Afford in 2026

Home Wealth Blueprint #2: Budgeting and Cash Flow - Know What You Can Comfortably Afford in 2026

This is Blog 2 of 9 - Financial Literacy for Confident Homeowners

→ View the full 9-part series here

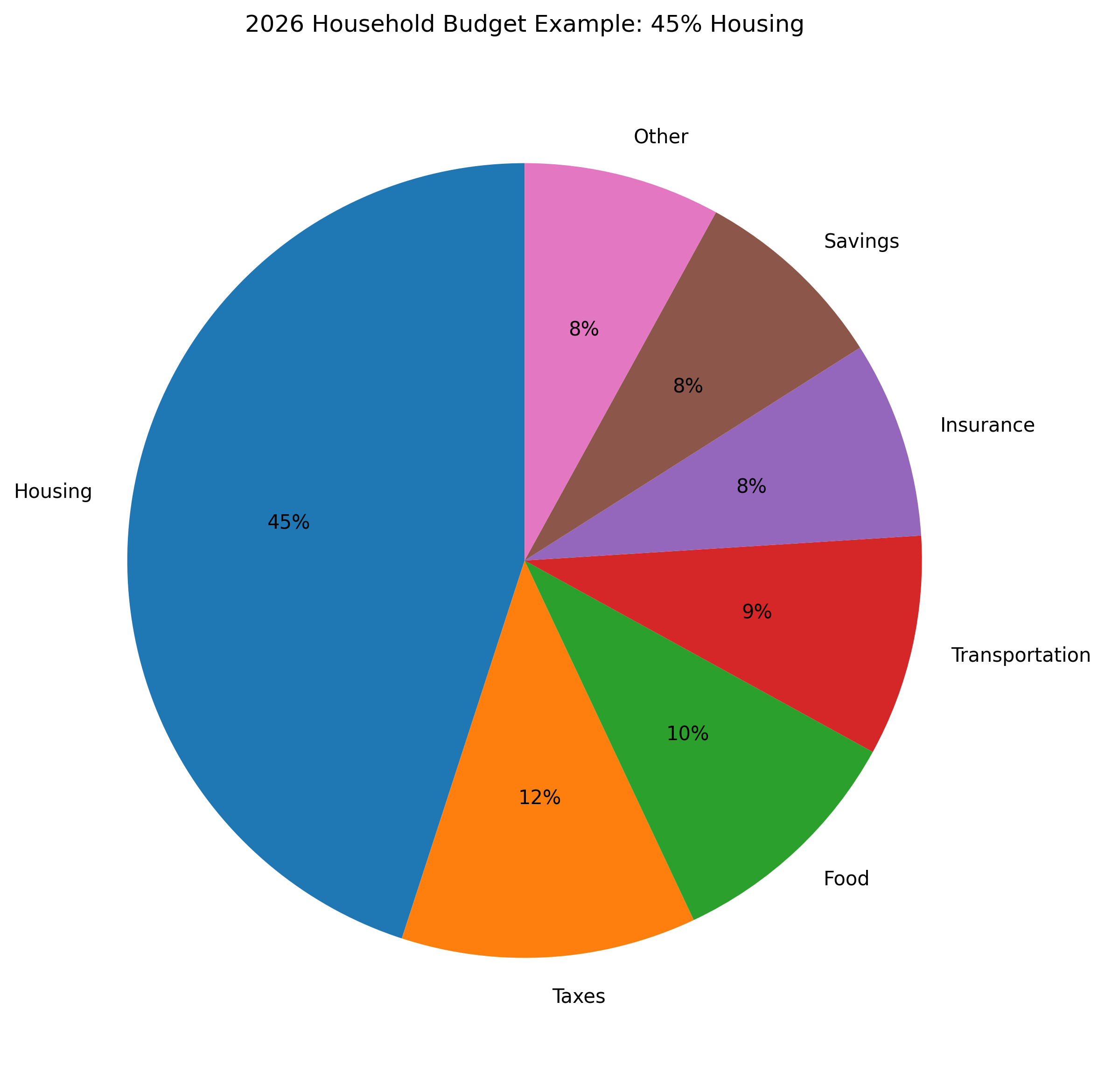

In 2026, housing costs (PITI) now average close to 45% of gross income for many families. This post shows you exactly how to build a realistic budget and know what you can comfortably afford.

Think About All the Surprises Life Has Already Given You

If you want to be prepared, it takes foresight and planning. When we work together, I share 40 years of lessons learned from helping thousands of families across California, Nevada, and Tennessee.

This is Blog 2 of the Home Wealth Blueprint series.

← Read Blog 1: Financial Literacy and Homeownership Overview

Why Budgeting Matters More Than Ever in 2026

Housing costs have risen. The average family now spends nearly 45% of gross income on principal, interest, taxes, and insurance (PITI). A solid budget helps you stay in control.

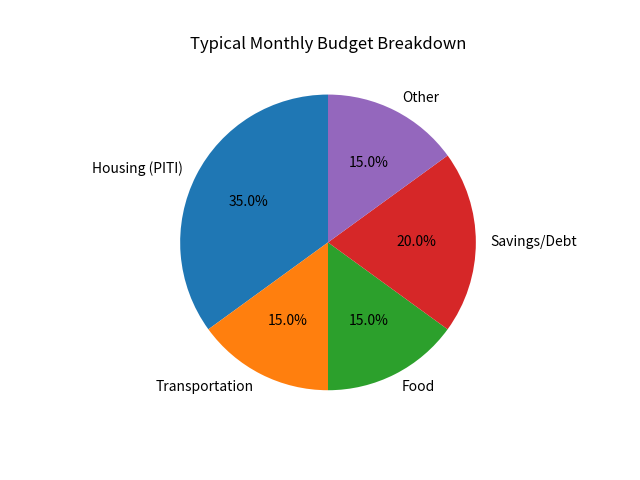

What Does a Healthy Housing Budget Look Like?

- Ideal: 28 - 35% of gross monthly income

- Maximum (stretch): 43 - 45% (lender approved but requires discipline)

- Red Flag: Over 45% - very little room for life's surprises

Debt-to-Income (DTI) Ratio Explained

Lenders look at two numbers:

- Front-end DTI: Housing costs only

- Back-end DTI: All debts + housing

Most programs prefer back-end DTI under 43%. We can often find solutions even if you're slightly above that.

Practical Budgeting Steps You Can Take Today

- Track every dollar for 30 days

- Separate needs vs. wants

- Build a 3 - 6 month emergency fund

- Run your real numbers with us (soft credit pull)

Ready to See What You Can Comfortably Afford?

Get a clear, realistic picture based on your full financial situation - not just what you might qualify for on paper.

Start Pre-Approval - California

Start Pre-Approval - Tennessee & Other Areas

Schedule a Quick Consultation with Steve

Coming Up Next in the Series

Internal Links for Further Reading

- First-Time Homebuyer Programs in California and Nevada

- Understanding Closing Costs and Escrow

- VA and USDA Loans Explained

Additional Resources

Tags: home wealth blueprint, budgeting for home buying, debt to income ratio, mortgage affordability 2026, California mortgage, Nevada mortgage, Tennessee mortgage, PITI explained, first time homebuyer