Home Wealth Blueprint #5: Debt Management – Using “Good Debt” to Build Wealth in 2026

Home Wealth Blueprint #5: Debt Management: Using Good Debt to Build Wealth in 2026

This is Blog 5 of 9: Financial Literacy for Confident Homeowners

View the full 9-part series here

Debt management is one of the most important parts of building long-term wealth through homeownership. Not all debt is bad. A well-structured mortgage can be "good debt" when it helps you build equity, protect monthly cash flow, and create more financial choices over time.

The key is knowing which debts help move you forward and which debts quietly drain your wealth. This post will help you think through mortgage debt, high-interest debt, 15-year versus 30-year loan choices, refinance options, HELOC strategies, and ways to reduce or remove mortgage insurance.

Think About All the Surprises Life Has Already Given You

If you want to be prepared, it takes foresight and planning. Life brings job changes, family changes, market changes, medical surprises, home repairs, and unexpected expenses. A smart debt management plan helps you stay flexible instead of feeling trapped by payments.

When we work together, I share 40 years of lessons learned from helping thousands of families across California, Nevada, and Tennessee. The goal is not just to get a loan closed. The goal is to help you understand how your mortgage fits into your bigger financial picture.

This is Blog 5 of the Home Wealth Blueprint series.

Read Blog 4: Credit Management |

Read Blog 3: Saving Strategies |

Read Blog 1: Overview

Debt Management Starts with Good Debt vs. Bad Debt

Good debt is debt that can help you build an asset, improve your financial position, or create future opportunity. A mortgage can be good debt because it gives you the ability to own a home, build equity, and potentially benefit from long-term appreciation.

Bad debt usually works the opposite way. High-interest credit cards, payday loans, and unnecessary consumer debt can drain monthly cash flow and make it harder to qualify for better mortgage options later.

A mortgage becomes excellent debt when you choose the right structure, understand the payment, protect your reserves, and stay ahead of your long-term goals.

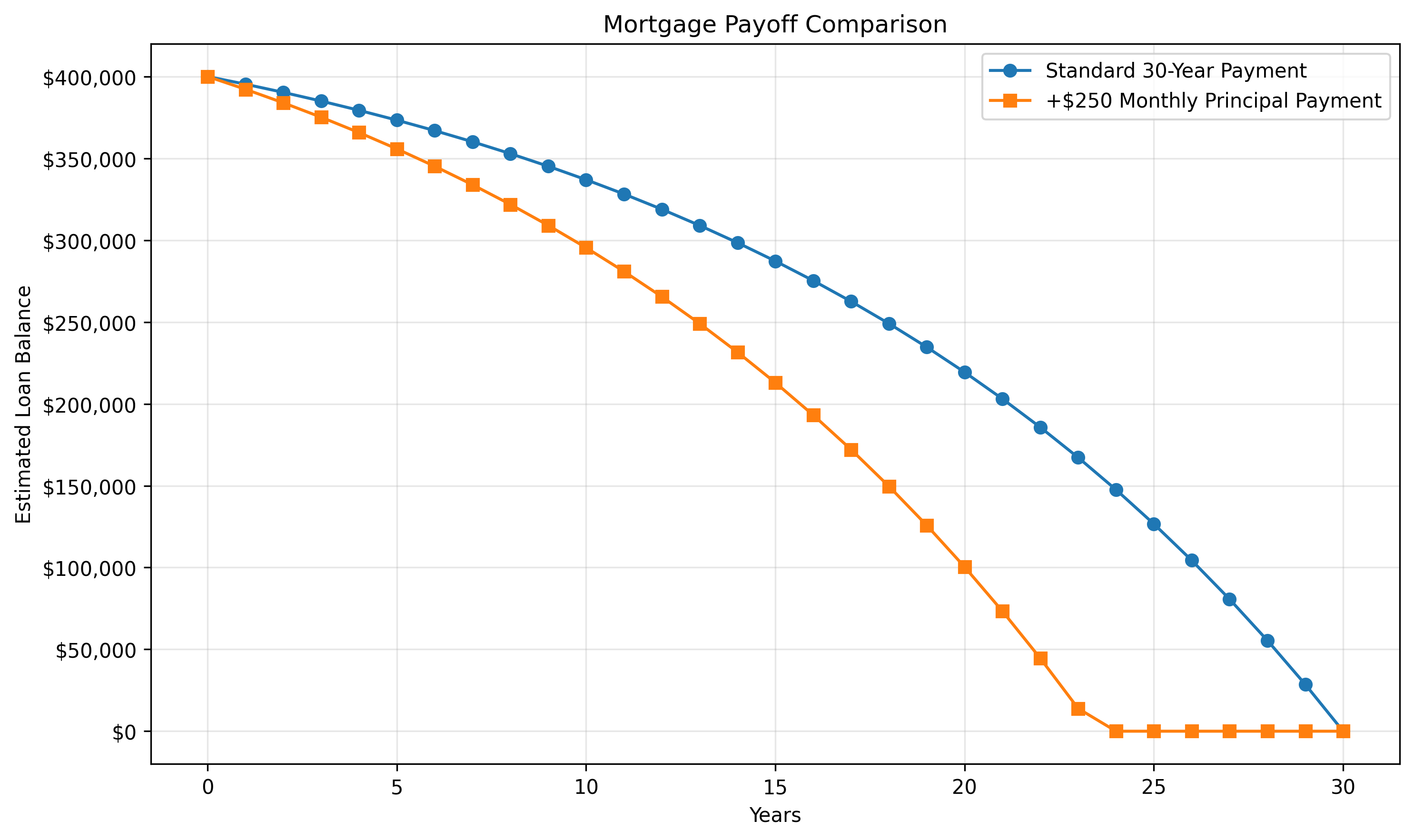

Debt Management and the 15-Year vs. 30-Year Mortgage Choice

One of the biggest debt management decisions homeowners face is whether to choose a 15-year mortgage, a 30-year mortgage, or a flexible hybrid strategy.

- 30-Year Mortgage: Lower required monthly payment and more flexibility.

- 15-Year Mortgage: Faster equity growth and less total interest over time.

- Hybrid Strategy: Start with a 30-year mortgage and make extra principal payments when your budget allows.

A 15-year loan may be attractive if your main goal is to pay the home off faster. A 30-year loan may be better if you want more flexibility, stronger monthly cash flow, or room for other financial priorities. The right answer depends on your income, savings, comfort level, family goals, and long-term plan.

Key Debt Management Strategies for Homeowners

- Keep your debt-to-income ratio under control. Your debt-to-income ratio, often called DTI, can affect your mortgage approval, buying power, and loan options.

- Pay more than the minimum when possible. Extra principal payments can reduce interest and shorten your payoff timeline.

- Protect your cash reserves. Paying down debt is helpful, but draining your savings can create risk if life changes unexpectedly.

- Consider refinancing when the numbers make sense. A refinance may help lower your payment, improve your loan structure, remove mortgage insurance, or consolidate higher-interest debt.

- Use a cash-out refinance or HELOC responsibly. Home equity can be powerful, but it should be used with a clear purpose and a repayment strategy.

- Avoid new high-interest debt after closing. New debt can weaken your monthly budget and make future mortgage planning harder.

When Refinancing or a HELOC May Help with Debt Management

Some homeowners carry high-interest debt while also having available home equity. In the right situation, a cash-out refinance or HELOC may help simplify payments, reduce monthly obligations, or create a more organized debt management plan.

That does not mean it is always the best move. The smart approach is to compare the total cost, monthly savings, loan term, interest rate, and long-term effect on your equity. The lowest payment is not always the best strategy, and the fastest payoff is not always the most comfortable strategy.

Before using home equity, it is important to compare the net cost of keeping your current mortgage and adding a second mortgage versus refinancing your current mortgage into a new first mortgage.

PMI and MIP: How to Eliminate Mortgage Insurance Faster

Private Mortgage Insurance on a conventional loan, or Mortgage Insurance Premium on an FHA loan, can add cost to your monthly payment. If your equity has improved, it may be worth reviewing whether that mortgage insurance can be reduced or removed.

Conventional PMI may be removable when you reach enough equity, depending on your loan and servicer rules. FHA mortgage insurance may require refinancing into another loan type if the numbers make sense. Either way, mortgage insurance should be part of your debt management review.

Ready to Turn Your Debt into Wealth?

Debt management is not about shame, pressure, or one-size-fits-all advice. It is about understanding your full financial picture and choosing a mortgage strategy that supports your goals.

We can review your current debt, mortgage options, refinance opportunities, PMI or MIP removal options, and long-term payoff goals. Then we can compare what fits best for you: lower payment, faster payoff, debt consolidation, stronger cash reserves, or a better overall plan.

Start Pre-Approval: California

Start Pre-Approval: Tennessee and Other Areas

Schedule a Quick Consultation with Steve

If any of your friends, family, or co-workers are looking to buy, sell, or refinance, can I count on you to introduce us via text or email?

Coming Up Next in the Series

Internal Links for Further Reading

- Refinance Options for Lower Payments or Cash-Out

- Understanding Closing Costs and Escrow

- VA and USDA Loans Explained

Additional Resources

One small favor: If any of your friends, family, or co-workers are looking to buy, sell, or refinance, can I count on you to introduce us via text or email?

Start Your Pre-Approval

Move from “shopping” to “offer-ready” in hours, not weeks.

Was this helpful?

If this guide added value, a quick Google review helps others find us.

Tags: home wealth blueprint, debt management, good debt mortgage, bad debt, mortgage payoff strategy, 15 year mortgage, 30 year mortgage, 15 vs 30 year mortgage, debt to income ratio, DTI mortgage, PMI removal, MIP removal, refinance strategy, refinance 2026, debt consolidation refinance, HELOC strategy, cash out refinance, home equity, build wealth with real estate, homeowner wealth strategy, mortgage planning, California mortgage, Nevada mortgage, Tennessee mortgage, Reno mortgage broker, Modesto mortgage broker, Knoxville mortgage broker, First Capital Mortgage Inc