Home Wealth Blueprint #7: Homeownership as the Cornerstone of Retirement and Wealth Building in 2026

This is Blog 7 of 9: Financial Literacy for Confident Homeowners

View the full 9-part series here

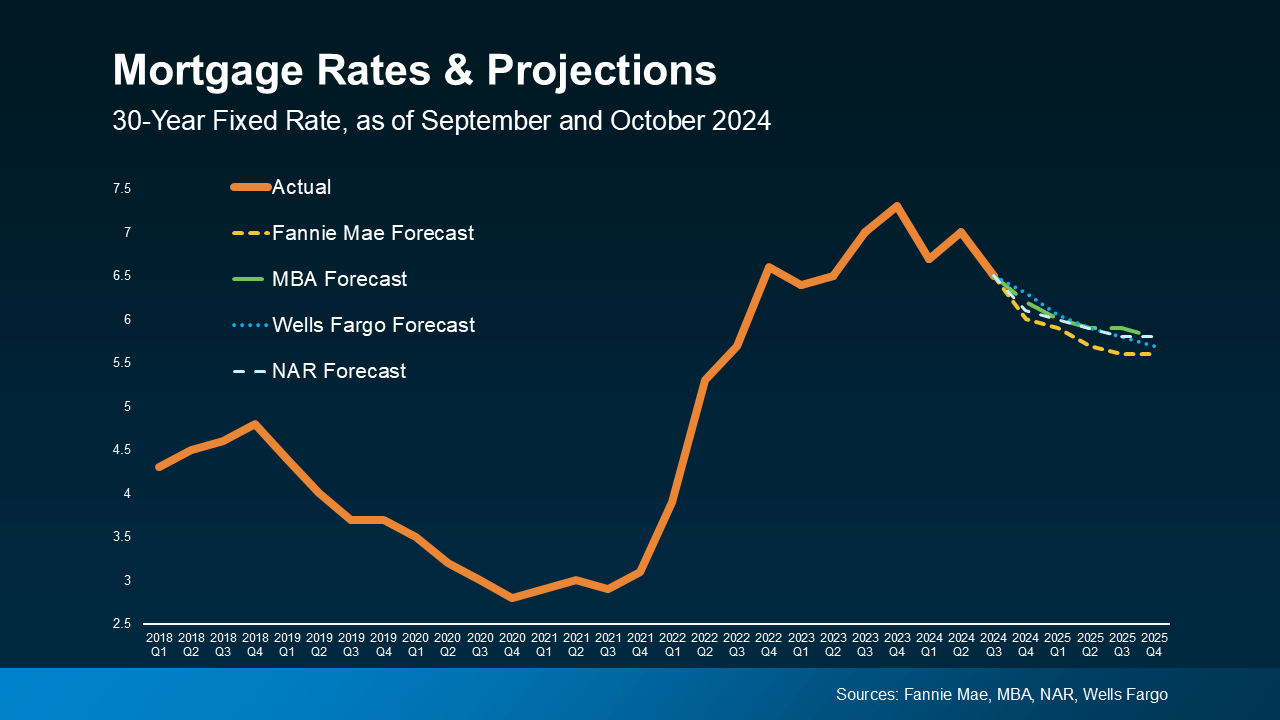

Homeownership and retirement planning work best when they are treated as one coordinated strategy.

Your home is often your largest asset and can become a powerful tool for creating retirement security, financial flexibility, and generational wealth. This guide explains how thoughtful mortgage and equity decisions can support your future.

Think About All the Surprises Life Has Already Given You

Preparing for the future takes foresight and planning. When we work together, I share 40 years of lessons learned from helping thousands of families across California, Nevada, and Tennessee.

Good financial decisions are not only about managing debt or reducing expenses. They can provide greater freedom, more lifestyle choices, and the ability to pursue the people, experiences, and goals that matter most to you.

This is Blog 7 of the Home Wealth Blueprint series.

Read Blog 6: Taxes, Insurance and Risk Management

|

Read Blog 5: Debt Management

|

Read Blog 1: Overview

How Homeownership and Retirement Planning Work Together

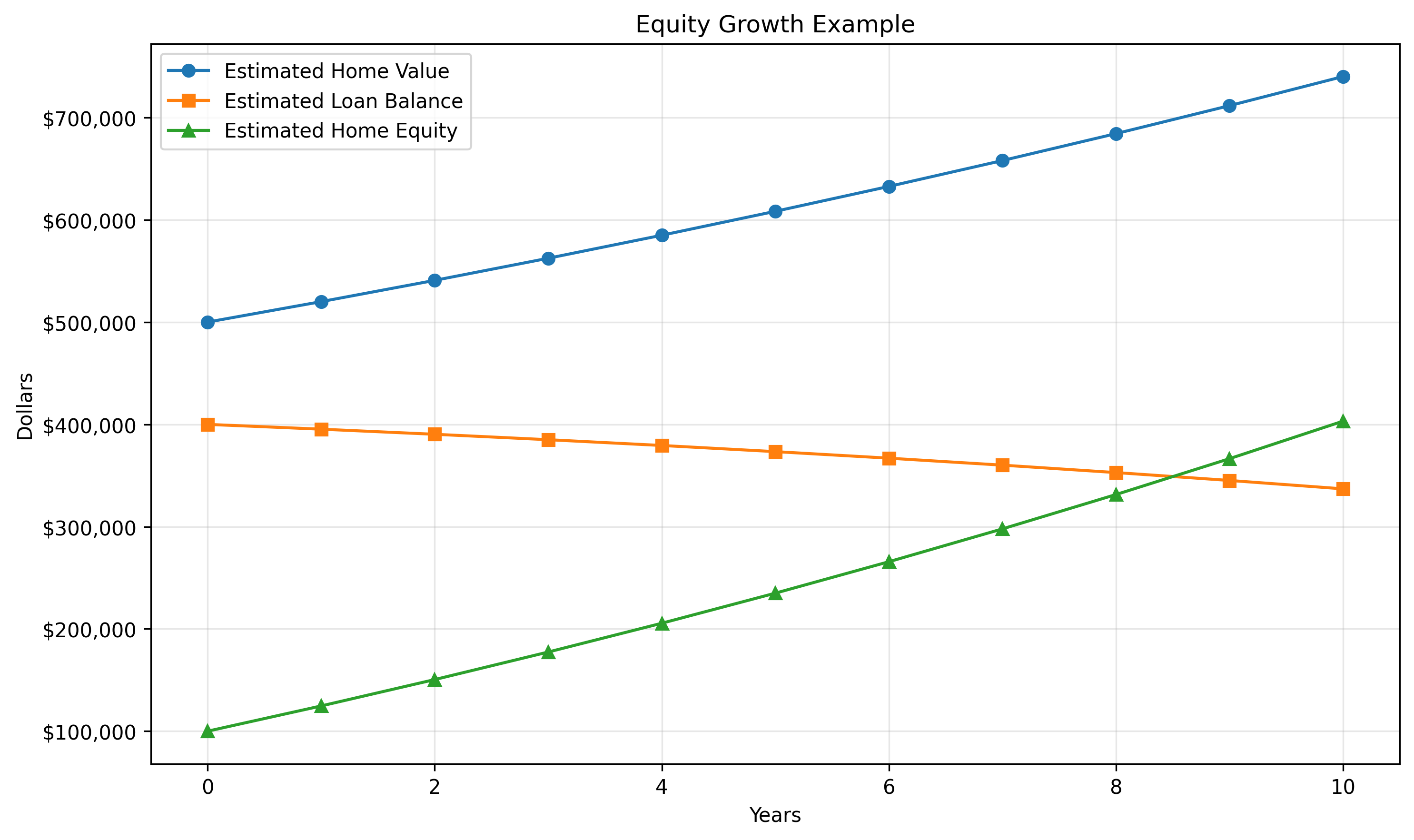

Unlike rent, mortgage payments can help build equity that you own. Over time, a combination of home appreciation and principal reduction may significantly increase your net worth.

Your home can also provide financial flexibility later in life. Depending on your circumstances, that flexibility might include lowering your monthly housing expense, accessing equity for important needs, downsizing, or creating a legacy for the next generation.

Home Equity Growth Over Time

Key Ways Homeownership Can Build Wealth

- Consistent savings through principal reduction:

A portion of each mortgage payment may increase the amount of the home you own. - Potential appreciation:

Home values may increase over time, although appreciation is never guaranteed. - Possible tax advantages:

Some homeowners may qualify for mortgage interest or property tax deductions. Consult a qualified tax professional regarding your individual situation. - Leverage:

Homeownership allows you to control a valuable asset without paying the entire purchase price in cash. - Financial flexibility:

Depending on your qualifications and available equity, refinancing, a home equity loan, or a HELOC may provide access to funds for important financial goals.

Strategic Mortgage and Equity Tools for Retirement

- Refinance to improve monthly cash flow:

A refinance may help lower the payment, change the loan term, or replace an existing loan with one that better fits your current goals. - Use equity strategically:

A cash-out refinance, home equity loan, or HELOC may provide funds for improvements, debt consolidation, healthcare expenses, or other major needs. - Consider downsizing:

Selling a larger home and purchasing a smaller property may help reduce expenses or free up equity for retirement. - Evaluate reverse mortgage options:

For eligible homeowners, a reverse mortgage may help supplement retirement income or increase monthly financial flexibility. - Plan for the mortgage payoff:

Some homeowners prioritize entering retirement without a mortgage, while others may benefit from keeping affordable financing and preserving liquid assets.

There is no single strategy that is right for everyone. The best approach depends on your income, available savings, current mortgage, home equity, retirement timeline, family responsibilities, and long-term lifestyle goals.

Generational Wealth Considerations

Proper planning can help your home become a valuable legacy asset rather than an unexpected responsibility for your children or grandchildren.

Important considerations may include how title is held, whether the home will be sold or retained, how an existing mortgage will be handled, and whether heirs will have the financial ability and desire to keep the property.

Mortgage planning should also be coordinated with appropriate legal, estate planning, tax, and financial professionals. Each professional provides a different part of the overall strategy.

Questions to Ask About Your Retirement Housing Strategy

- Will my current mortgage payment remain comfortable after retirement?

- How much equity do I currently have?

- Would paying off the mortgage reduce too much of my available cash?

- Could refinancing improve my monthly cash flow?

- Would downsizing support the lifestyle I want?

- Should I preserve the home as part of my family legacy?

- Could a home equity loan, HELOC, or reverse mortgage help meet future needs?

- Have I coordinated my mortgage strategy with my tax, financial, and estate plans?

Ready to Make Your Home Work Harder for Your Future?

Homeownership and retirement planning are personal.

The right strategy depends on your current mortgage, available equity, retirement timeline, income needs, family goals, and the lifestyle you want to create.

We help clients review mortgage and equity strategies that align with their retirement goals, financial priorities, and family legacy plans. A thoughtful review can help you understand your available options without assuming that borrowing against your home is automatically the right solution.

Start Pre-Approval: California

Start Pre-Approval: Tennessee and Other Areas

Schedule a Quick Consultation with Steve

Know someone who could benefit from a thoughtful mortgage conversation?

If any of your friends, family, or co-workers are looking to buy, sell, or refinance, can I count on you to introduce us via text or email?

Coming Up Next in the Series

Further Reading

Refinance Options for Lower Payments or Cash-Out

Home Equity Loans and HELOCs

VA and USDA Loans Explained

Additional Resources

Tags:

home wealth blueprint, homeownership and retirement planning, homeownership retirement, building equity, generational wealth, home appreciation, refinance strategy, HELOC, mortgage payoff strategy, downsizing in retirement, California mortgage, Nevada mortgage, Tennessee mortgage