Refinancing in 2026: Create Your Plan and Strike Rate – Before Rates Drop

Thinking About Refinancing in 2026? Now Is the Time to Create Your Refinance Plan

Many homeowners are feeling the pressure of higher monthly payments and a still-uncertain economic environment. If you've been waiting for the right time to refinance, current forecasts offer cautious optimism.

I've been helping homeowners with mortgage strategy for over 40 years, and one thing I can tell you is this: the best time to prepare for a refinance is before the market gives you the rate you want - not after.

Right now, many industry forecasts suggest mortgage rates could gradually improve over the next several months. That does not mean you should sit and watch the market every day. It means you should build a smart plan now so you are ready to act when the opportunity shows up.

Why Homeowners Are Watching Rates More Closely in 2026

Homeowners across California, Nevada, Tennessee, and beyond are still feeling the impact of higher interest rates, rising costs, and tighter monthly budgets. For some, refinancing could mean lowering a payment. For others, it may be a way to consolidate debt, remove mortgage insurance, shorten the loan term, or improve long-term cash flow.

Not every homeowner should refinance today. But many homeowners should be preparing now so they can move quickly when the numbers make sense.

What a Strike Rate Means for Your Refinance Strategy

One of the smartest ways to prepare - without constantly checking rates or reacting emotionally to headlines - is to establish your personal strike rate.

Your strike rate is the interest rate at which refinancing clearly makes sense for you based on your current loan, your monthly savings, your closing costs, your timeline in the home, and your overall financial goals.

Once that rate becomes available, you are ready to act quickly and confidently.

That is far more effective than guessing, waiting for news stories, or hoping someone else tells you the perfect moment to move.

Refinancing Is Not Just About the Rate

Many people think refinancing is only about getting the lowest rate possible. In reality, a smart refinance strategy looks at the full picture.

Your refinance may be about:

- Lowering your monthly payment

- Reducing total interest over time

- Paying off higher-interest debt

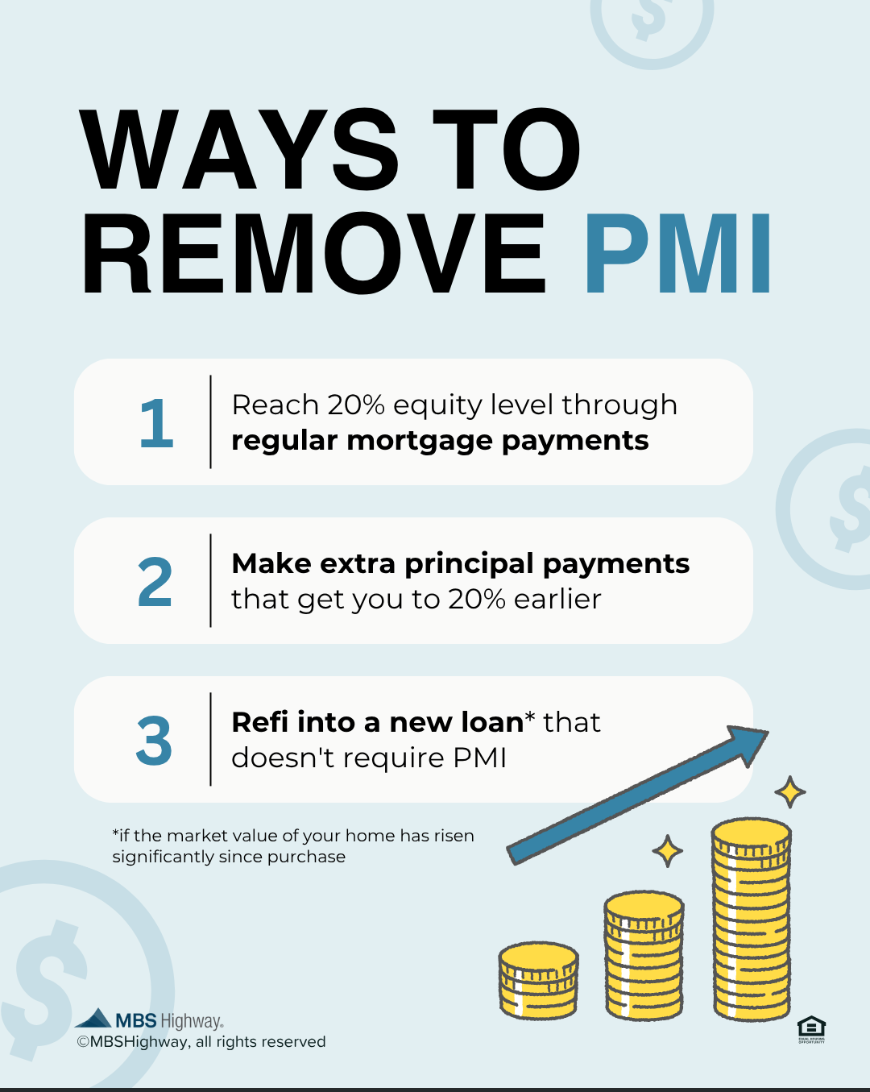

- Removing FHA mortgage insurance when eligible

- Changing from an adjustable-rate loan to a fixed-rate loan

- Shortening your loan term to build equity faster

The right strategy depends on your current mortgage, your financial goals, and how long you plan to keep the home.

Why a Simple Refinance Plan Can Save You Time and Stress

Most homeowners do not want to spend time analyzing markets, reading conflicting forecasts, or trying to calculate break-even points on their own. They want a clear answer to one question: When does refinancing make sense for me?

That is where a personalized refinance plan becomes valuable.

In a short conversation, we can review your current loan, estimate your ideal strike rate, outline potential savings, and help you understand what to watch for. That way, when the right opportunity appears, you already know your next step.

You Do Not Have to Figure This Out Alone

At First Capital Mortgage Inc., my team and I help homeowners create refinance strategies that are practical, personal, and easy to understand. Whether you are hoping to reduce your payment, improve cash flow, or simply be ready when the market shifts, we are here to help.

You do not need pressure. You need clarity, a smart plan, and someone who knows how to help you move when the timing is right.

Let's Build Your Personalized Refinance Plan

If you'd like help creating your refinance plan, let's connect. In just 15 minutes, we can map out your ideal strategy, run the numbers, and position you to take advantage of the opportunity when it arrives.

Take the Next Step

Whether your goal is a lower payment, improved cash flow, debt consolidation, or simply being ready when rates improve, we can help you build a refinance plan that fits your situation.

Refinance FAQ for Homeowners

1. How do I know if refinancing makes sense for me?

Refinancing usually makes sense when it helps you achieve a clear goal, such as lowering your payment, reducing interest over time, removing mortgage insurance, or consolidating higher-interest debt. The right answer depends on your current rate, loan balance, closing costs, and how long you plan to stay in the home.

2. What is a strike rate in refinancing?

A strike rate is the interest rate at which refinancing becomes clearly worthwhile for your specific situation. Instead of guessing, you define that target in advance so you can act quickly when the market reaches it.

3. Should I wait to refinance until rates drop more?

Sometimes waiting makes sense, but waiting without a plan can cause missed opportunities. A better approach is to review your current loan now, identify your strike rate, and be fully prepared so you know exactly when refinancing is worth it.

Start Your Pre-Approval

Move from “shopping” to “offer-ready” in hours, not weeks.

Was this helpful?

If this guide added value, a quick Google review helps others find us.